The ‘cloud AI wars’ at major technology companies are intensifying (Goldman, 2022). Industry leaders say AI is transforming society. AI’s foundational and transformative nature is emphasised by Bill Gates (2023) and Alphabet’s Sundar Pichai (2023). Amazon, Microsoft, and Google are allegedly driving this transformation. Cloud computing has created the socio-technical infrastructure for expansive growth and platform capitalism, enabling their ‘hyper-scalability’ (Narayan, 2022).

Discursively, ‘AI’ attracts significant investments and drives AI startups to partner with Amazon, Microsoft, and Google (Alphabet), which ‘pour billions’ into expensive cloud computing (Hodgson, 2023). These tech giants support and invest in infrastructure to establish themselves as infrastructure providers. For strategic, political, and economic reasons, understanding AI value chains in the digital platform economy is crucial as AI enters its ‘industrial age’ (The Economist, 2022).

AI as an existing technology stack and ecosystem

The meaning of ‘AI’ is ambiguous and changing. Crawford (2021) emphasizes that ‘how we define AI, what its boundaries are, and who determines them’ shapes our perceptions and frames debates. Raley and Rhee (2023) suggest viewing AI as ‘an assemblage of technological arrangements and socio-technical practices, as concept, ideology, and dispositif’ while remaining ‘attuned to actually existing socio-technical systems’ in critical AI studies. Jacobides et al. (2021) and Rieder (2022) recommend viewing AI as a large technical system and focusing on its technical details and materials to understand its operations and power.

In line with these perspectives, we view AI as a technology stack and (emerging) ecosystem as well as a discursive phenomenon (Gillespie, 2010). The AI technology stack includes infrastructure, models, applications, and their providers. Manufacturers of cloud software and hardware platforms benefit from the AI market. According to digital platform theory (Jacobides et al., 2021; de Reuver et al., 2018; Van der Vlist, 2022), the AI stack ecosystem includes third-party developers and businesses’ apps and solutions.

These elements either technically complement the cloud platform stack or represent a group of firms and organizations working together with its components. The ‘sectoral and national systems of firms and institutions that collectively engage in [AI]’ in China, the US, and the EU are evolving differently, with ‘a handful of firms building global AI ecosystems’ (Jacobides et al., 2021). Variations in these national or sectoral systems highlight AI’s political economy, intricate supply chains, dependencies, and third parties’ role in its creation, capture, and commercialization.

A technography of cloud AI

We use critical platform and algorithm studies and ‘technography’ to examine Big Tech’s role in artificial intelligence industrialization and cloud infrastructure dependency. This descriptive and interpretive approach critiques technical system structure and operation (Bucher, 2016; Mackenzie, 2019; Van der Vlist et al., 2022). Technography encourages direct reading of publicly available technical system documents to examine technology’s material aspects.

Technical documentation, developer and product site reliability engineers, financial reports, media articles, press releases, and blog posts explain technical systems’ goals, functions, and capabilities. This lets us explain specific technology features while criticizing promotional language and industry jargon in these materials.

We scope Big Tech’s AI Infrastructure monitoring support and investments, including partnerships, acquisitions, and financial investments. This approach lets us identify prominent examples of infrastructural support and investments essential to AI industrialization. We focus on Amazon, Microsoft, and Google due to their market dominance and industry influence (Richter, 2023). We don’t compare their cloud platforms, but we acknowledge their similarities and differences.

Big Tech’s infrastructural support and investments in AI

Our analysis first examines Amazon, Microsoft, and Google’s corporate partnerships, acquisitions, and financial investments to demonstrate the importance of infrastructure in AI industrialization. OpenAI and Stability AI receive attention but rely heavily on Big Tech support and investment. These companies have built strong partnerships, invested heavily, and acquired AI companies and initiatives (Murgia, 2023). Many AI firms have exclusive or preferred cloud partnerships with Big Tech due to financial and infrastructural needs for scaling AI models and applications.

Big Three companies invest heavily. According to Crunchbase and Tracxn, Microsoft has made 211 investments and 214 acquisitions, spending over $188 billion on acquisitions. Google has made 238 investments and 260 acquisitions, spending $41.8 billion. Amazon has invested 132 times and acquired 99 times, spending $36.9 billion.

Big Tech’s infrastructural support and investments in AI

Our analysis first examines Amazon, Microsoft, and Google’s corporate partnerships, acquisitions, and financial investments to demonstrate the importance of infrastructure in AI industrialization. OpenAI and Stability AI receive attention but rely heavily on Big Tech support and investment. These companies have built strong partnerships, invested heavily, and acquired AI companies and initiatives (Murgia, 2023). Many AI firms have exclusive or preferred cloud partnerships with Big Tech due to financial and infrastructural needs for scaling AI models and applications.

Big Three companies invest heavily. According to Crunchbase and Tracxn, Microsoft has made 211 investments and 214 acquisitions, spending over $188 billion on acquisitions. Google has made 238 investments and 260 acquisitions, spending $41.8 billion. Amazon has invested 132 times and acquired 99 times, spending $36.9 billion.

Surveying cloud offerings

The technical documentation for AWS, Microsoft Azure, and GCP’s extensive cloud offerings shows their views on AI and machine learning and their cloud infrastructure connections.

Microsoft’s ‘Azure Machine Learning’ and ‘Azure AI Content Safety’, Amazon’s ‘AWS Deep Learning AMIs’, and Google’s ‘Document AI’ and ‘Vision AI’ are examples of cloud products and services that use ‘AI’, ‘ML’, and ‘Deep Learning’ in their titles or descriptions. Many titles describe the service’s purpose without using these terms, such as AWS’s ‘Fraud Detector’ and ‘Transcribe’, Azure’s ‘Bot Services’ and ‘Speech to text’, and GCP’s ‘Recommender’. Hardware infrastructure services like Google’s ‘Cloud GPUs’, ‘Cloud TPUs’, and ‘Deep Learning VM Image’ provide processing units and preconfigured virtual machines for machine-learning applications. This shows that AI and machine learning are essential components integrated across categories, emphasizing the need for a holistic view.

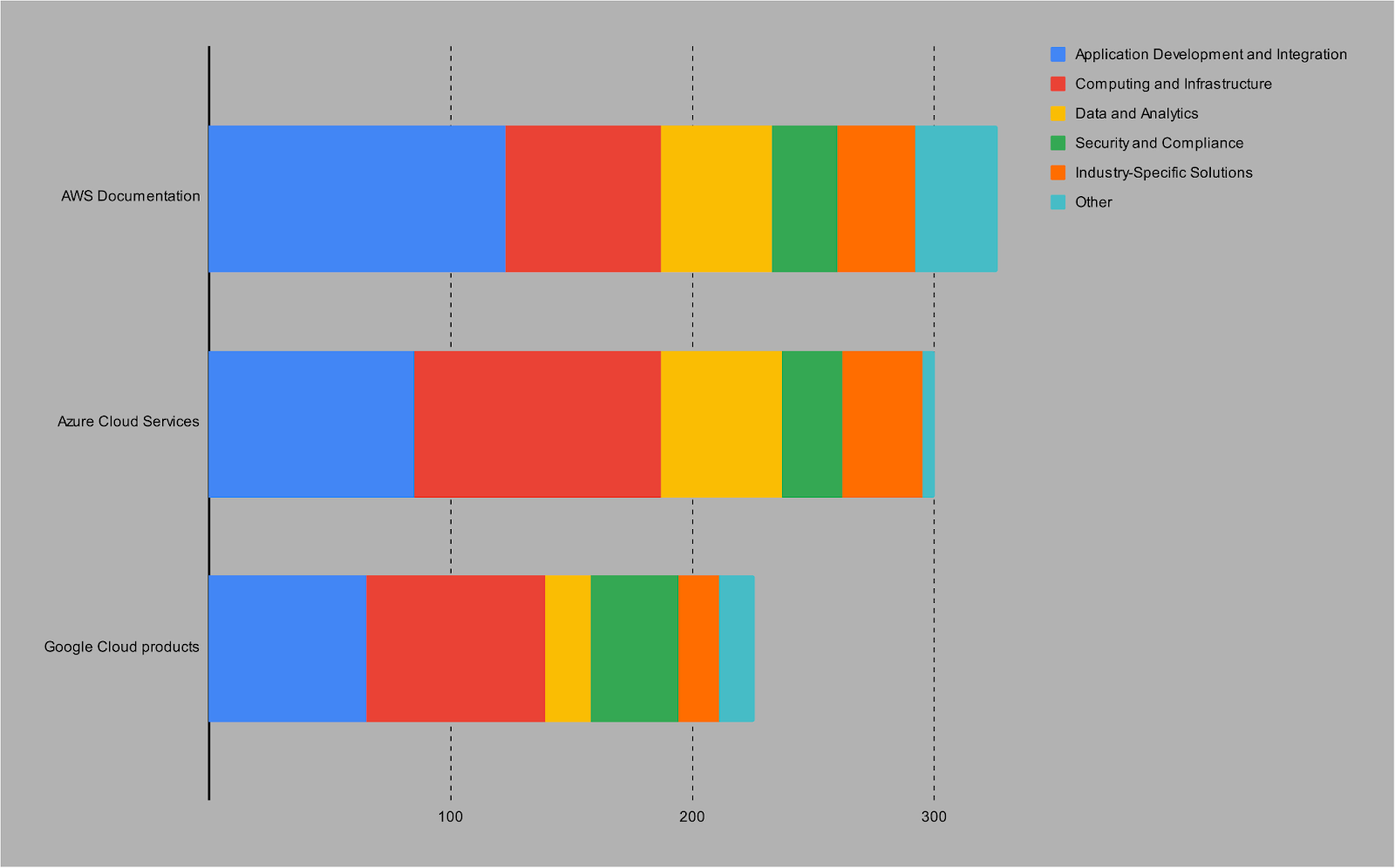

First, the Application Development and Integration category (273 products) covers developer, integration, and management tools. Google’s Cloud Functions, a serverless execution cloud environments for building and connecting cloud services, and Azure’s Logic Apps, a cloud service for automating workflows and integrating systems, are examples. Second, the Computing and Infrastructure category (240 offerings) includes compute, containers, storage, serverless computing, databases, and networking. Amazon Elastic Compute Cloud (EC2), Azure’s Virtual Machines, and Google Kubernetes Engine are notable offerings.

Security and Compliance includes identity and access management, compliance, and cryptography. AWS Identity and Access Management, Azure Active Directory, and GCP’s are examples. The Industry-Specific Solutions category (82 products) caters to financial services, healthcare, media and gaming, and the Internet of Things. Google’s ‘Cloud Healthcare API’ manages healthcare data, and Azure’s ‘Media Services’ encodes, streams, and protects media. The Other category (54 offerings) includes ‘AWS Ground Station’ for satellite communication and control, ‘AWS RoboMaker’ for robotics, and ‘Azure Lab Services’ for cloud-based virtual machine labs for teaching, training, and testing.

AI and cloud platforms

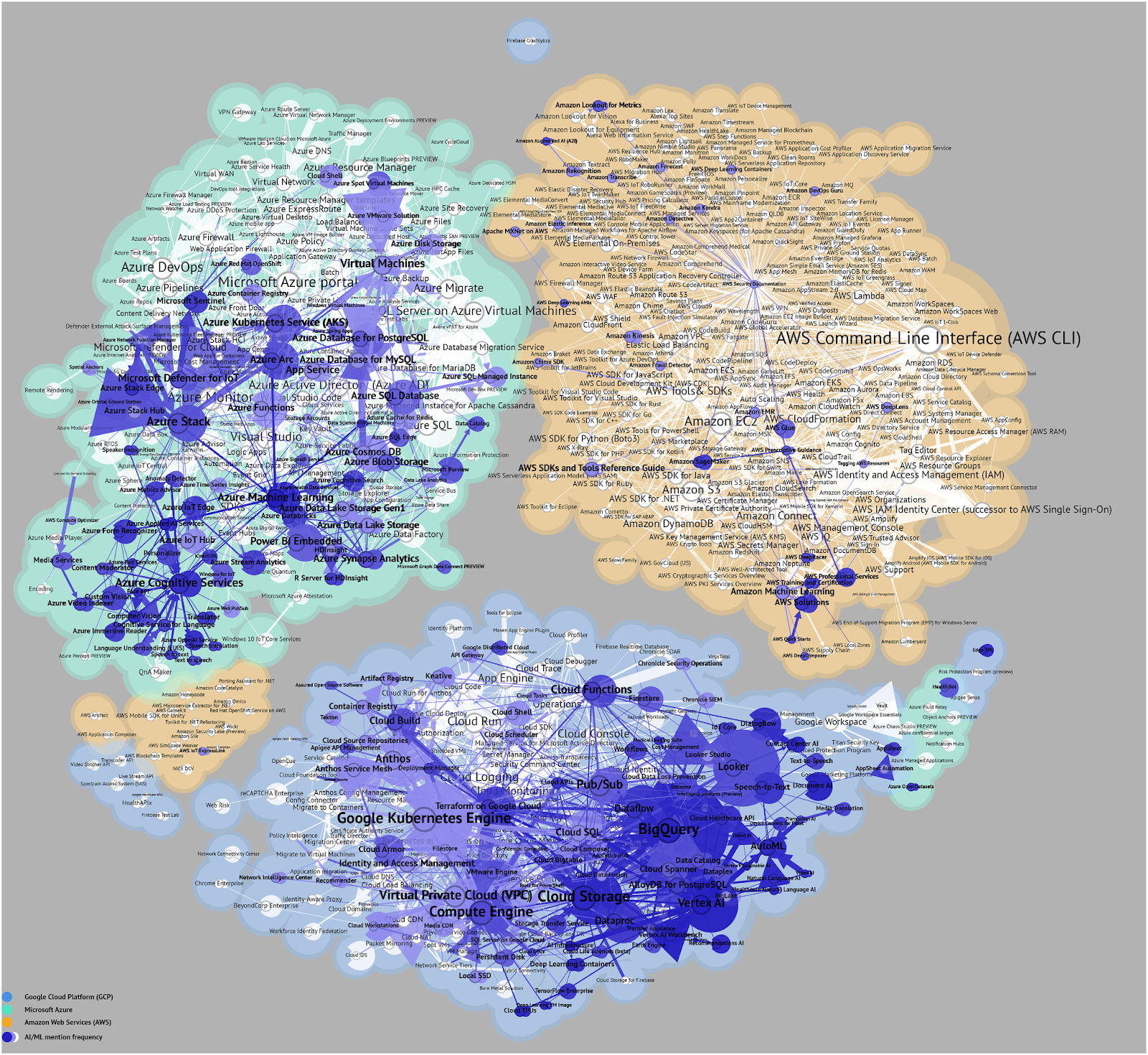

The extensive documentation on these tools, products, and services shows how crucial cloud platform components are interconnected. These companies’ public technical platform documentation is an exhaustive catalog. This documentation helps enterprise software developers understand and implement these diverse services by providing detailed specifications for each offering and frequent technical citations and references to related offerings. GCP’s ‘Vertex AI’ documentation describes integration options and functionalities like exporting datasets from ‘BigQuery’, creating custom machine-learning models with ‘BigQuery ML’, using the integrated development environment in ‘Vertex AI Workbench’, generating data labels with ‘Vertex Data Labeling’, and optimizing training time and costs with ‘AI Infrastructure’. Azure and AWS platform documentation have similar structures. These citations and references in each product’s documentation provide a complete picture of the AWS, Azure, and GCP cloud platform ecosystems.

By color-coding product documentation pages by the frequency of ‘AI’ and machine-learning mentions (AI/ML), we can identify AI/ML-related products (nodes) and clusters. This creates a visual ‘heatmap’ overlay showing AI/ML mention density per offering and its stack-wide prominence. This approach includes products that use AI/ML terminology in their descriptions or technical specifications. Azure mentions AI/ML in 36.8% of their product documentation, indicating a significant presence. GCP has 49.2% of its products referencing AI/ML, while AWS has 9%.

Industry-specific and marketplace solutions

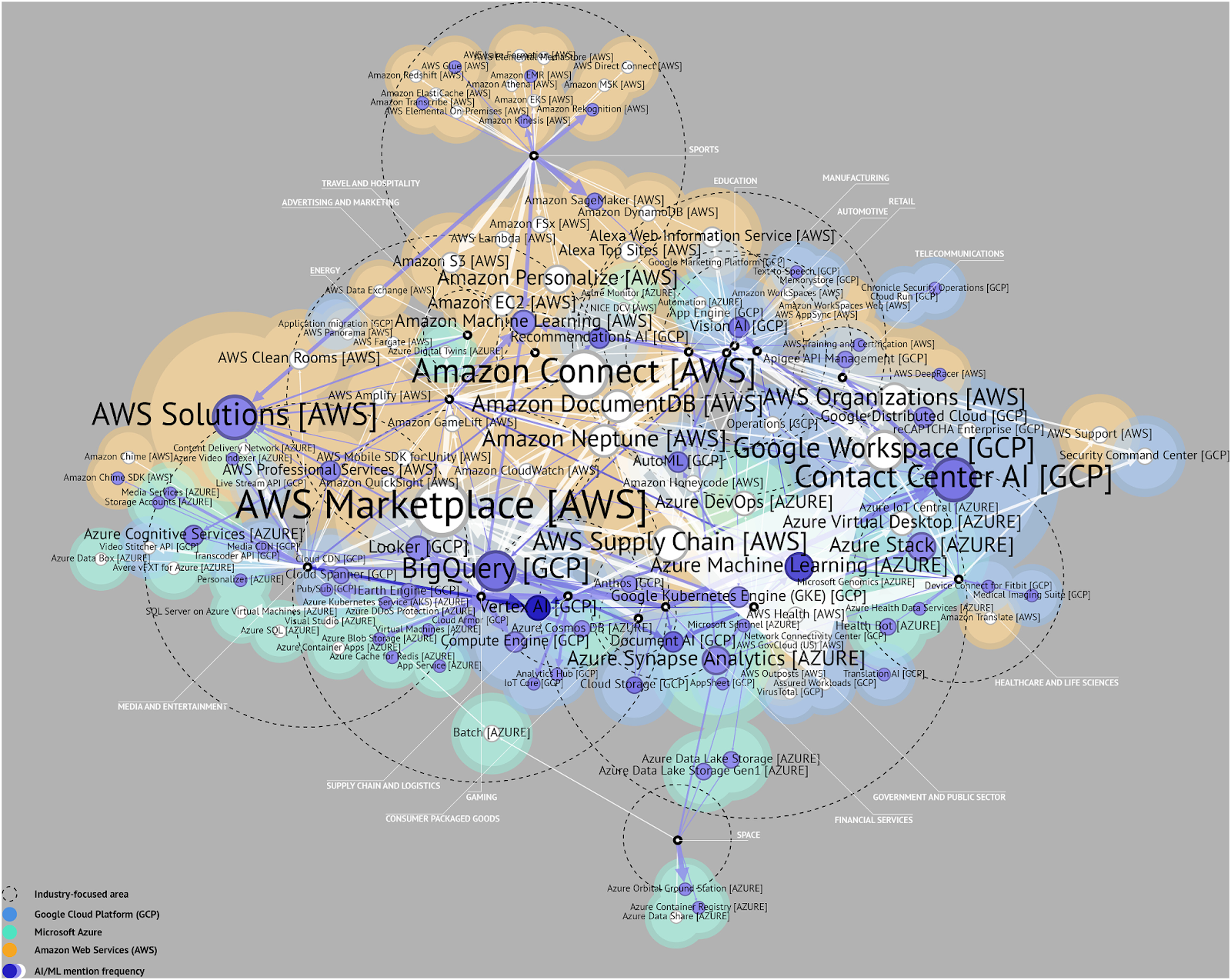

We also found specialized cloud offerings for specific industries with unique needs. These industry-specific AI tools, products, and services have dedicated documentation pages. Government and Public Sector, Education, Healthcare, Gaming, Media and Entertainment, Advertising and Marketing, Energy, Manufacturing, Automotive, Retail, Financial Services, and Supply Chain and Logistics are among these target industries. We can find product-industry sector associations by detecting product citations in these industry-specific documentation pages. This method provides another view of cloud AI stack interconnectedness.

The interconnected citation network shows which industries cloud platforms target. The ‘Cloud Healthcare API’, ‘Medical Imaging Suite’, and ‘Healthcare Natural Language AI’ from GCP enable AI solutions for medical diagnostics and data analysis. Azure offers ‘Health Data Services’, ‘Azure Data Lake Storage’, and a ‘Health Bot’ for AI-powered virtual healthcare assistants, while AWS offers ‘AWS Health’ and ‘HealthLake’ for machine-learning-based medical and insurance data transformation.

‘Discovery AI for Retail’ and ‘Recommendations AI’ improve retail conversion rates and provide personalized product recommendations. For customer interaction and contact centers, Amazon Connect and GCP’s Contact Center AI are available. Data management and analysis are supported by BigQuery, Amazon DocumentDB, and Azure Synapse Analytics. Azure Machine Learning, Azure Machine Learning, and GCP’s Document AI offer machine-learning capabilities. Amazon Neptune and Google Workspace provide graph databases and productivity tools for schools and businesses.

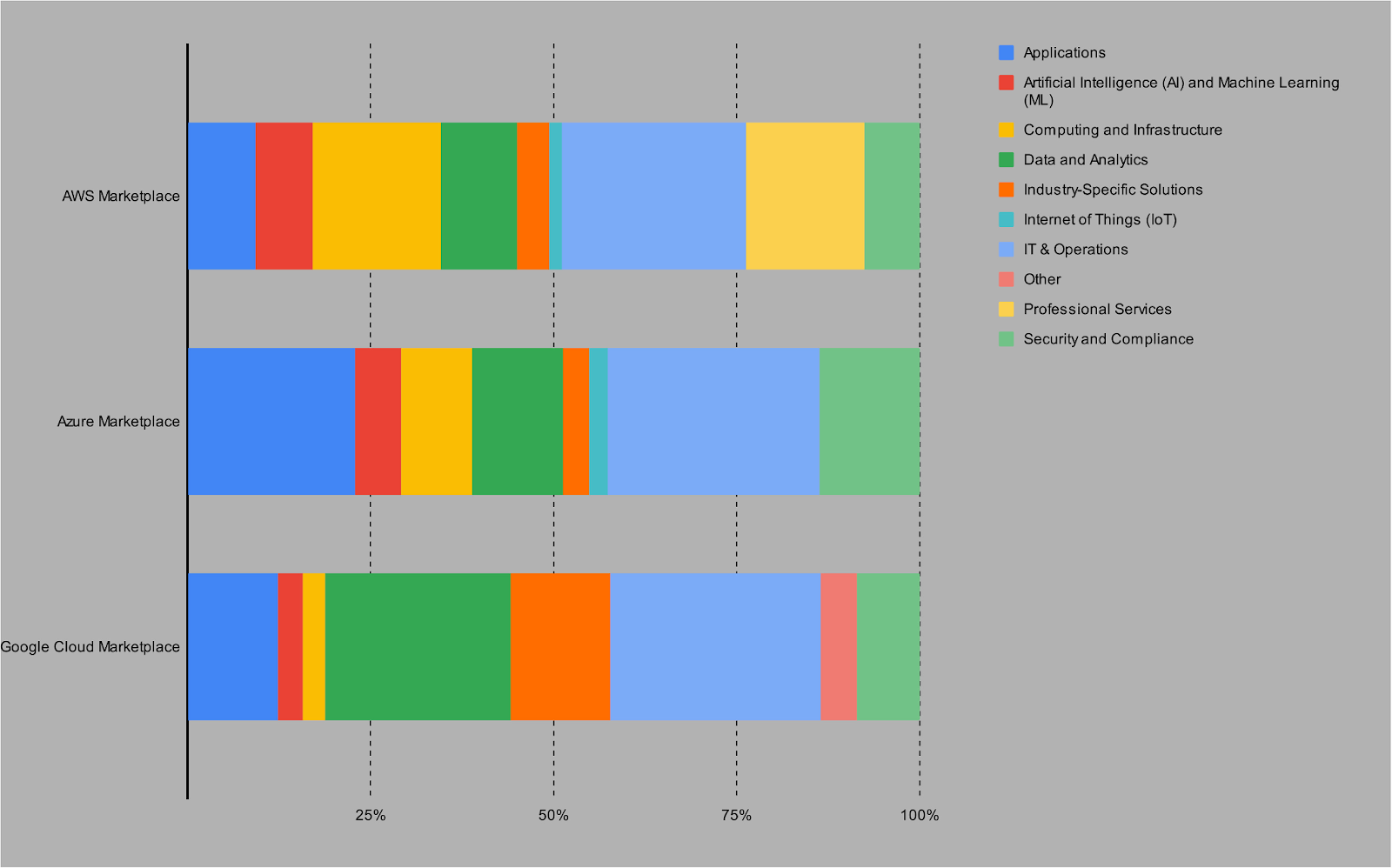

A quick look at AWS, Azure, and Google Cloud solutions yields intriguing insights. Shows the significant differences in marketplace app numbers across categories between these marketplaces. Azure has 39,857 apps, AWS 32,987, and GCP 6387.

AWS Marketplace has many offerings in (business) applications (7420), AI and ML (7051), computing and infrastructure (23,000), data and analytics (8655), industry-specific solutions (3777), IoT (1411), IT & operations (18,225), professional services (12,231), and security and compliance (3460). AI and ML (2410), computing and infrastructure (3768), data and analytics (4783), industry-specific solutions (1396), IoT (971), IT & operations (11,226), and professional services (5280) are strong Azure Marketplace areas. Google Cloud Marketplace emphasizes data and analytics (1615), industry-specific solutions (876), IoT (218), and IT & operations (312). These findings show that Azure, AWS, and GCP marketplaces can meet a variety of customer needs with their diverse and deep offerings.

AI’s industrialisation and cloud infrastructure dependence

This study examined the roles of Amazon, Microsoft, and Google (Alphabet) in the ‘industrialization of artificial intelligence’. We used a two-pronged technographic approach to understand their AI infrastructure support and investments, followed by a thorough analysis of their cloud platform products and services. We viewed AI as a technology stack and ecosystem as it moved from research to commercial products and services, acknowledging its discursive role. The implications of widespread cloud infrastructure use are discussed below.

We found significant infrastructural support and investments through partnerships, investments, and acquisitions in our first analysis. Smaller players must actively seek Big Tech collaborations. Strategic alliances, partner programmes, and financial investments create new constraints and ‘lock-in’ effects tied to leading technology companies’ infrastructure and support (Dyer-Witheford et al., 2019). Partner programs and strategies orchestrate platform ecosystems, attracting third-party developers and businesses to create applications and solutions, especially those tailored to specific industries, driving AI industrialization (Egliston and Carter, 2022; Helmond et al., 2019). These programs strengthen these platforms’ infrastructure and strategy in the emerging AI ecosystem (Van der Vlist and Helmond, 2021).

Big AI beyond Amazon, Microsoft, and Google

Other AI giants like Oracle, Adobe, IBM, and Salesforce could be studied alongside Amazon, Microsoft, and Google. These companies specialize in data management (‘Oracle Data Cloud’ and ‘Salesforce Data Cloud’), marketing clouds (‘Adobe Experience Cloud’), and customer relationship management (‘Salesforce Einstein GPT’) and have significant influence in the ecosystem (Van der Vlist and Helmond, 2021). They provide industry-specific services and solutions and some use hyperscale computing architectures.

Industry-specific AI solutions from these intermediaries help expand cloud and AI providers. Cloud platform providers’ clientele and market reach vary across industries and regions, according to publicly available data (Paraskevopoulos, 2023). Oracle is popular in South America, Microsoft is preferred by large corporations and manufacturing companies, and Google is preferred by smaller companies, especially in ICT. These findings show that AI industrialization platforms have different niches in the global AI market.

While the AI ecosystem goes beyond the Big Three, their support and investments are crucial. Hugging Face, a leading open-source AI community platform, facilitates machine-learning model and project collaboration. what is Retrieval Augmented Generation? Hugging Face’s strategic partnership with AWS shows its continued dependence on major technology companies’ infrastructure (Kak and Myers West, 2023). Many American, Chinese, and European companies and startups collaborate with and contribute to the global AI landscape (Jacobides et al., 2021). Although these players often depend on or are acquired by Big Tech, their sector-specific solutions help industrialize AI and deserve more attention.

Conclusion

Major tech companies are fighting the ‘cloud AI wars’ as AI transforms society and drives investments. This transformation is driven by Amazon, Microsoft, and Google investing billions in infrastructure to become infrastructure providers. AI infrastructure, models, applications, and providers make up an emerging ecosystem. Microsoft has spent over $188 billion on AI infrastructure acquisitions and Google $41.8 billion. These companies invested heavily, formed strong partnerships, and acquired AI companies and initiatives.

AWS, Microsoft Azure, and Google’s cloud offerings’ technical documentation discusses AI, machine learning, and cloud infrastructure connections. Applications development and integration, computing and infrastructure, security and compliance, industry-specific solutions, and more are available. Understanding AI value chains in the digital platform economy is crucial as AI enters its ‘industrial age’.

Google, Amazon, and Microsoft’s extensive AI and cloud platform documentation show their interconnectedness. Developers can understand and implement diverse services using these platforms’ detailed specifications, technical citations, and related offerings. Cloud services for government, education, healthcare, and other industries are also available. Azure, AWS, and GCP marketplaces offer business applications, AI and ML, computing and infrastructure, data and analytics, industry-specific solutions, IoT, IT & operations, professional services, and security and compliance. Strategic alliances, partnerships, and acquisitions push AI industrialization, with smaller players seeking Big Tech partnerships. Oracle, Adobe, IBM, and Salesforce also provide industry-specific services and solutions to the ecosystem. Hugging Face and other American, Chinese, and European companies contribute to the global AI ecosystem.

{kind=link}